3 stages of retirement – and how to plan for your income needs in each

Your priorities — and spending — will likely change as you move through retirement. Here’s how to prepare.

Travel? Volunteering? More time with loved ones? You probably have an idea of your perfect retirement. But don’t count on it staying the same over what could be a period of more than 30 years.

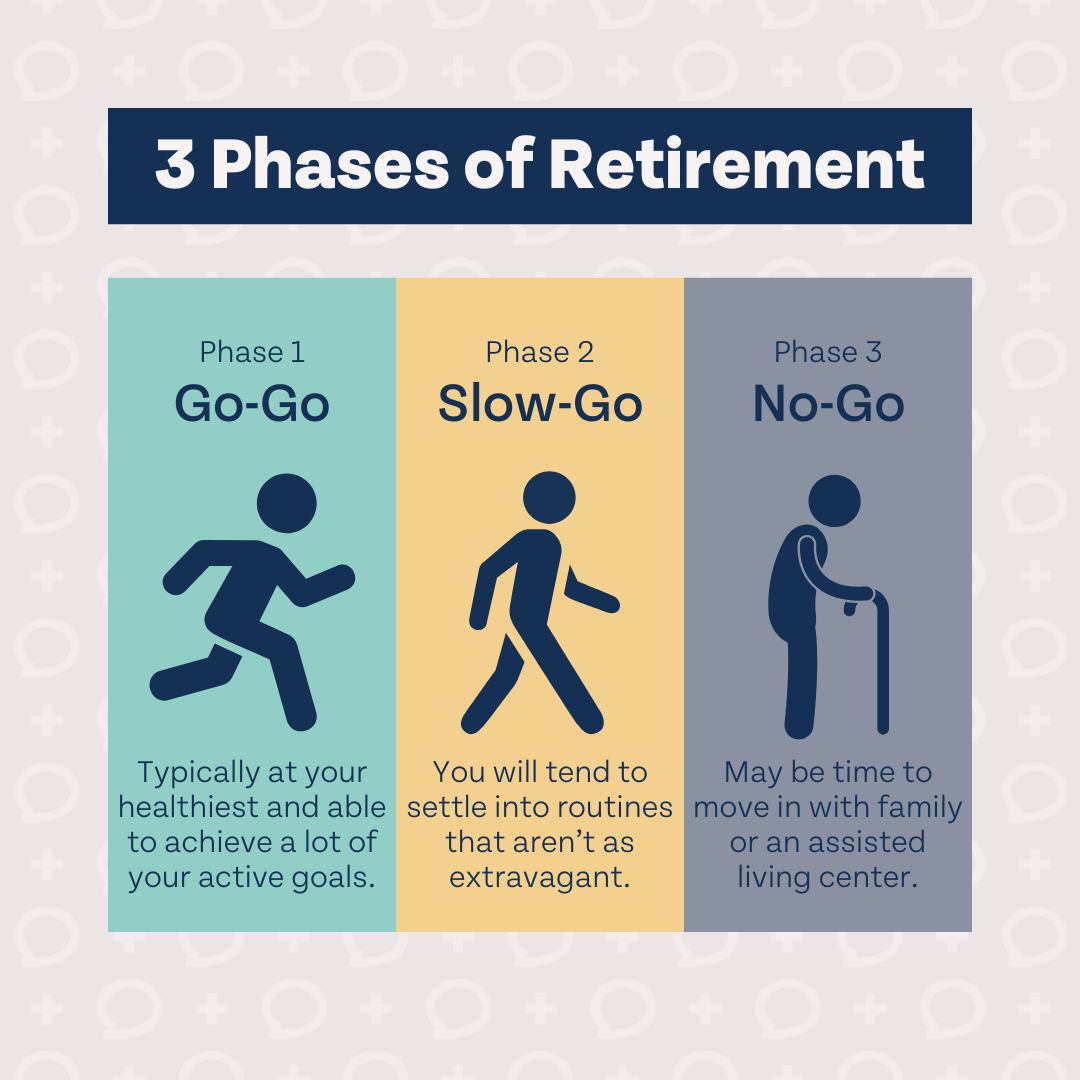

Most people go through three stages of retirement. In the first — let’s call it the Exploring stage — you’re likely going to try new things and pursue your passions and hobbies. You might later transition to the Nesting stage, with more predictable routines and a greater focus on home and family. And later comes a Reflecting stage, where health issues and your legacy assume prime importance.

“It’s critical to understand how your income needs and spending habits will change. That way you can work with your advisor to create a flexible plan for each of these stages,” says Debra Greenberg, director, Personal Retirement, Investment Solutions Group at Bank of America. Below, take a look at how your retirement may evolve over time and what you can do to prepare.

Exploring

In the first stage of retirement, you might:

- Travel the world, learn new skills, volunteer and take up new hobbies.

- Move to a new locale and/or purchase a second home.

- Start a new business or work part time.

Steps you can take to prepare

Key financial priorities include continuing to invest for growth and future health care costs while also funding increased spending on leisure activities like travel. Ask an advisor:

- How can I develop a predictable income stream to cover both my essential and discretionary expenses?

- When should I consider taking Social Security benefits?

- How can I make tax-efficient withdrawals on my retirement accounts?

- What strategies should I consider to help protect myself against increased medical costs as I age?

Nesting

In the next stage, you may:

- Settle into a routine with a more relaxed pace.

- Travel closer to home or to see friends and family.

- Consider relocating or downsizing.

Steps you can take to prepare

As your spending slows a bit, consider using this period to prepare for potentially higher expenses in the next stage when you may face inflation and rising health care costs. Strategies to ask your advisor about include:

- Should I invest more aggressively to increase the odds that I won’t outlive my assets?

- What do I need to think about when renovating my home or relocating?

- Will I be ready to cover the cost of long-term care services if I need them later on?

Reflecting

In this stage, you could:

- Encounter more health-related expenses.

- Be a widow or widower, or need support from your family or others.

- Start thinking more deeply about your estate plan.

Steps you can take to prepare

You may want to strike a balance between securing your own financial future and leaving a legacy. Discuss the following with your advisors:

- Can my current withdrawal strategy cover the cost of any additional help I may need?

- Are my will, power of attorney, healthcare directive and beneficiaries on insurance and retirement accounts all up to date?

- Should I consider gifting some of my assets now?

Retirement can be divided into three main stages, each with its own unique financial needs and lifestyle considerations. Here’s a breakdown of these stages and how to plan for your income needs in each:

1. Early Retirement (Exploring Stage)

Age Range: 65-75

Lifestyle: This is often the most active phase. You might travel, pursue hobbies, volunteer, or even work part-time.

Income Planning:

Invest for Growth: Continue to invest to ensure your savings grow to cover future expenses.

Withdrawal Strategy: Develop a plan to draw down your assets, ensuring a predictable income stream. This might include Social Security benefits, pensions, annuities, and withdrawals from retirement accounts like IRAs and 401(k)s.

Healthcare Costs: Start planning for future healthcare expenses, as these can be significant.

2. Middle Retirement (Nesting Stage)

Age Range: 76-85

Lifestyle: Activities may slow down, and you might spend more time at home or with family. Health issues may start to become more prominent.

Income Planning:

Adjust Spending: Reevaluate your budget to reflect changes in lifestyle and health needs.

Healthcare and Long-term Care: Allocate more funds towards healthcare and potential long-term care needs.

Stable Income: Ensure your income sources remain stable and sufficient to cover both essential and discretionary expenses.

3. Late Retirement (Reflecting Stage)

Age Range: 86 and beyond

Lifestyle: This stage often involves more reflection and less activity. Health care becomes a primary concern.

Income Planning:

Simplify Finances: Simplify your financial affairs to make management easier.

Healthcare and Support: Ensure you have adequate funds for healthcare, long-term care, and any support services you may need.

Estate Planning: Focus on estate planning to ensure your assets are distributed according to your wishes.

Planning for these stages involves a balance between enjoying your retirement and ensuring you have enough resources to cover your needs as they evolve. It’s a good idea to work with a financial advisor to tailor a plan that fits your specific situation and goals.