Why parents should consider IUL as college savings vehicle?

Let’s say you have been investing into 529 college plans for your children, and your children receive a full scholarship for their 4-year college.

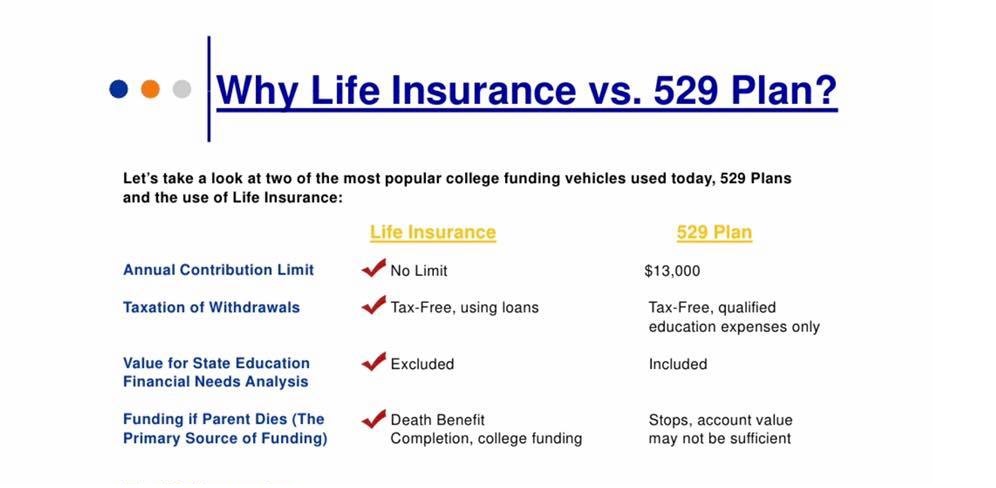

1. With 529, you have to pay TAXES on the money you take out. Also, you have to use it for EDUCATIONAL purposes ONLY, or pay 10% penalties(*) if you would like to use it for something else.

With IUL, you do NOT have to pay tax on the money you take out. Also, you can use the money for whatever you want.

2. 529 plans have market risk, it means you could LOSE money if the market goes down.

With IUL, you will gain interest when the market is up, but will NOT lose money when the market is down.

3. With 529, you will REDUCE your Financial Aid package.

With IUL, life insurance doesn’t include in Financial Aid analysis. So, you are SAFE.